Concept of Related Parties (Art. 179)

Two or more persons are considered related parties when one participates directly or indirectly in the management, control or capital of the other, or when a person or group of persons participates directly or indirectly in the management, control or capital of such persons. In the case of joint ventures, the members of the joint venture are considered related parties, as well as the persons who, in accordance with this paragraph, are considered related parties of such member.

Related Parties of a Permanent Establishment (Art. 179)

Related parties of a permanent establishment are considered to be the parent company or other permanent establishments of the same, as well as the persons mentioned in the preceding paragraph and their permanent establishments.

Art.76 sections IX and XII of the Income Tax Law mentions that persons who carry out transactions with related parties are obliged to determine the amount of their accumulated income and authorized deductions of such transactions considering the prices and amounts of consideration that would have been agreed with or between independent parties in comparable transactions, as well as to maintain and keep the corresponding supporting documentation (Transfer Pricing Study).

On the other hand, the tax authorities may exercise their verification power with respect to the income and deductions that should have been derived from such transactions in those cases in which the taxpayer does not have the support required by law.

The 2023 tax reform incorporated relevant changes regarding transfer pricing in the Income Tax Law (LISR) and the Federal Tax Code (CFF):

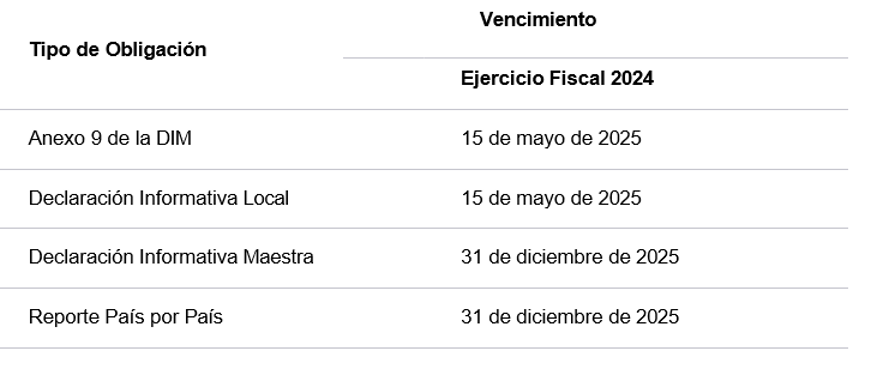

Deadlines

As a result of the changes made to articles 76, section X and 76-A of the LISR and 32-H of the CFF, the due dates applicable to each obligation as of 2023 are modified:

TRANSFER PRICING INFORMATIVE STATEMENTS

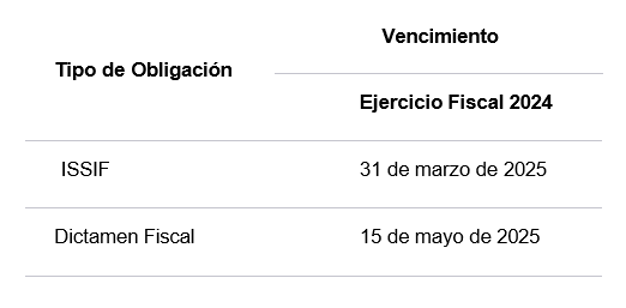

In addition to the aforementioned transfer pricing informative returns, taxpayers that are required to file the Information on the tax situation (ISSIF) or the Tax Report, must disclose transfer pricing information as part of the related party transactions sections. For these obligations, the due dates to be considered based on the reform under discussion are as follows:

TAXPAYERS OBLIGED TO COMPLY WITH THE LOCAL AND MASTER INFORMATIVE DECLARATION.

Article 32-H of the CFF incorporates section VI, which establishes that related parties of taxpayers obligated to file tax returns with taxable income over $1,062,919,860 MXN in fiscal year 2024 are also obligated to file the Local and Master Informative Declaration.

In previous years, the LISR established differences between the documentary requirements regarding transfer pricing for transactions with related parties resident in Mexico and abroad, so it is relevant to note that as of 2022 such distinctions are eliminated and the requirements are applicable to all transactions with related parties regardless of their place of residence.

Also, Articles 182 and 183 Bis of the Income Tax Law eliminate the option for maquiladoras to request an Advance Pricing Agreement (APA); as a result, taxpayers operating under maquiladora schemes will only be able to apply the Safe Harbor rule to comply with the transfer pricing rules for their maquila operations.

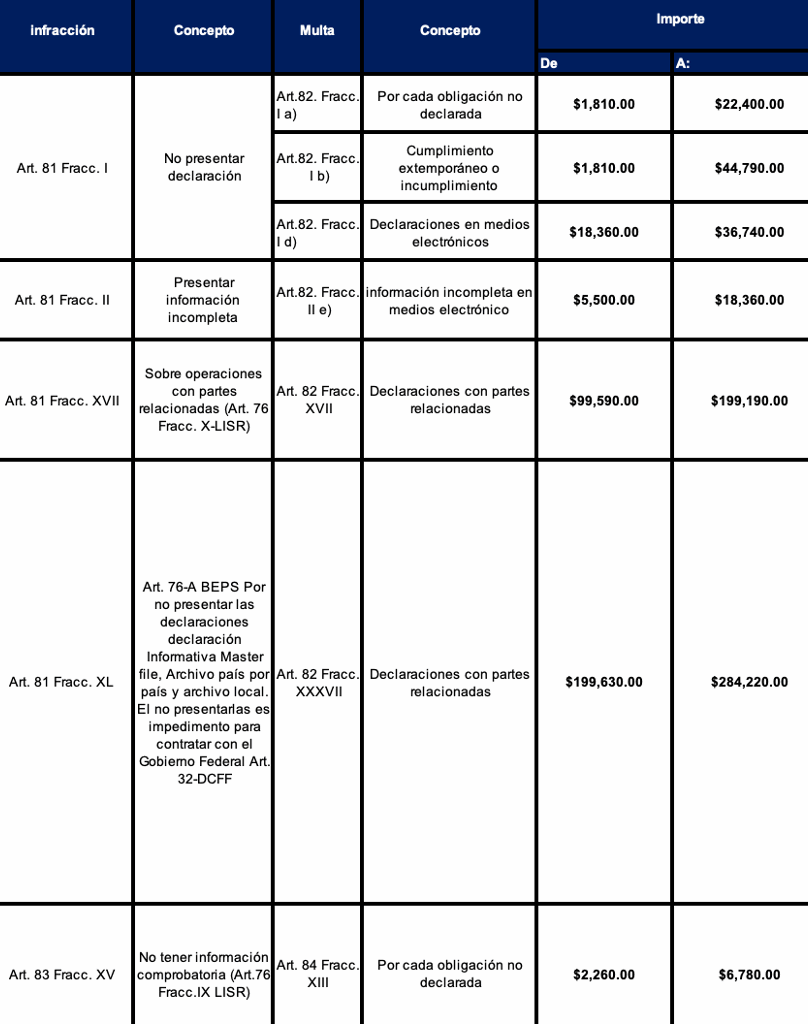

ESTABLISHED PENALTIES

Therefore, it is important to comply with everything related to this important tax issue of Transfer Pricing, obtaining and keeping the necessary supporting documentation to comply with the tax requirements and avoid unnecessary fines and violations.